Excess Liability vs. Umbrella Insurance: What’s the Difference?

As your family’s assets grow, adding extra liability coverage beyond what traditional home and auto insurance provides becomes more necessary. Policies like excess liability and umbrella insurance address that need by offering potential reimbursements beyond what those foundational plans provide when circumstances call.

While both options overlap or offer similarities, a few key distinctions allow each solution to address specific needs. In this explanation, we demystify the differences between excess liability and umbrella insurance products, making the choice easier and assisting individuals in choosing the appropriate insurance to protect their financial health and ensure peace of mind.

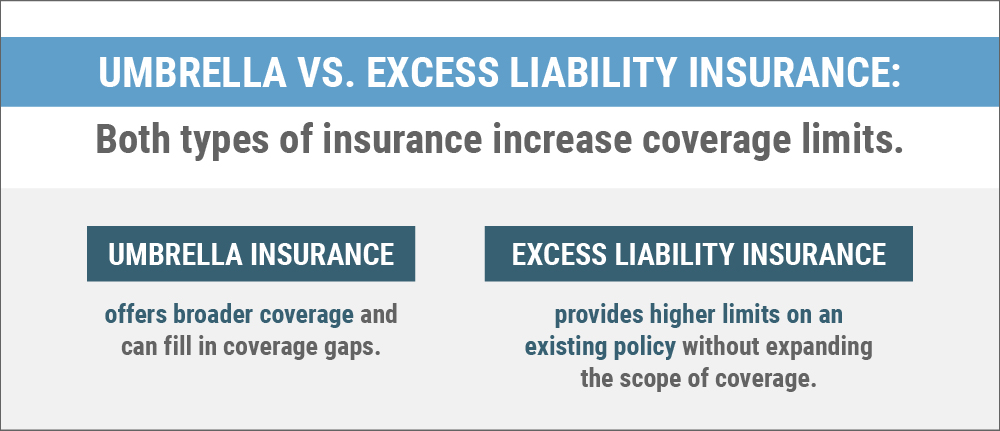

WHAT IS UMBRELLA INSURANCE?

Let’s start with umbrella insurance for individuals. Think of this type of insurance as an additional layer of personal protection coverage that kicks in after your primary coverage reaches its maximum payout. For example, if you get into an auto accident and become liable for $350,000 in damages, but your base policy only covers $250,000, your umbrella insurance may reimburse your family for the remaining $100,000.

This type of coverage is referred to as umbrella insurance because it may offer broader liability coverage extending beyond one event and even provide coverage outside of what’s stipulated in the underwriting. In other words, this insurance acts as an umbrella covering multiple circumstances instead of one, which is where excess liability coverage comes in.

WHAT IS EXCESS LIABILITY COVERAGE?

Excess liability coverage functions similarly to umbrella insurance, yet it offers customization based on specific situations. This type of insurance adheres to the terms and conditions of the original policy, meaning it extends coverage within the same scope, much like an umbrella, and follows the guidelines of the underlying insurance it supplements. For instance, when excess liability is added to auto insurance, the additional coverage is governed by the stipulations outlined in the primary policy.

UMBRELLA VS EXCESS LIABILITY INSURANCE

Both options offer additional liability coverage beyond primary insurance policies, such as auto and homeowners insurance. Here is how our insurance team differentiates both products—even if people use these terms interchangeably:

COVERAGE TYPE:

- Umbrella Insurance: May offer coverage that supports a range of circumstances beyond what’s outlined in a primary policy—like an umbrella covering multiple plans.

- Excess liability Coverage: Follows the rules outlined in the plan it endorses.

WHAT’S COVERED:

- Umbrella Insurance: Bodily harm, property damage, legal fees, and other lawful or physical liabilities.

- Excess Liability Coverage: Bodily harm, property damage, legal fees, and other lawful or physical liabilities associated with the policy it endorses.

PAYMENTS:

- Umbrella Insurance: Reimbursements kick in once one or several policies meet their limit.

- Excess Liability Coverage: Starts once the policy it endorses reaches its payment limit.

COVERED PARTIES:

- Umbrella Insurance: Offers coverage to individuals or entities associated with the policyholder, such as spouses and families.

- Excess Liability Coverage: May extend coverage to individuals or entities named explicitly in the policy, such as family members, spouses, and employees.

USE CASES:

- Umbrella Insurance: Potentially covers a broader range of circumstances and may provide additional coverage for events not listed under the primary policies it supports.

- Excess Liability Coverage: Recommended for individuals with significant assets or requiring elevated protection against specific risks for high-income earners.

Depending on your needs and circumstances, these insurance options could be the only resource to protect your financial well-being if you fall liable under catastrophic circumstances.

Remember, this is additional insurance that covers qualified expenses supporting you and your family beyond the limits of your primary insurance policies. That’s why we recommend it to our customers with assets or a net worth exceeding the liability limits of their foundational plans.

EXCESS LIABILITY OR UMBRELLA INSURANCE: WHICH IS RIGHT FOR YOU?

Like many insurance products, it depends. Below are a few questions we ask our partners when assessing their needs.

- Do you hold a personal policy for certain risks and want to increase your coverage?

- Consider excess liability insurance.

- Do you have a general liability policy covering several risks or need broader coverage?

- Consider umbrella insurance.

- Do you have gaps in your foundational policies that may not cover the excess amounts or want to increase liability coverage?

- Talk through both options.

We recommend consulting with your insurance provider to discuss coverage and to determine which product aligns with your needs and circumstances. Our experts create policies individualized to your needs based on the information provided.

We encourage you to learn more by contacting us online or calling us directly at (800) 735-8325. We look forward to speaking with you!

{kind=link}