What is Landlord Insurance & What Does It Cover?

Every investment property owner understands it takes the ability to make sound judgments and quick decisions to succeed. Part of that process involves securing landlord insurance that minimizes worries and maximizes savings.

Whether you’re a first-time landlord or a proprietor with a portfolio of several properties, continue reading to learn why holding a landlord policy fortifies your financial future.

WHY IS LANDLORD INSURANCE IMPORTANT?

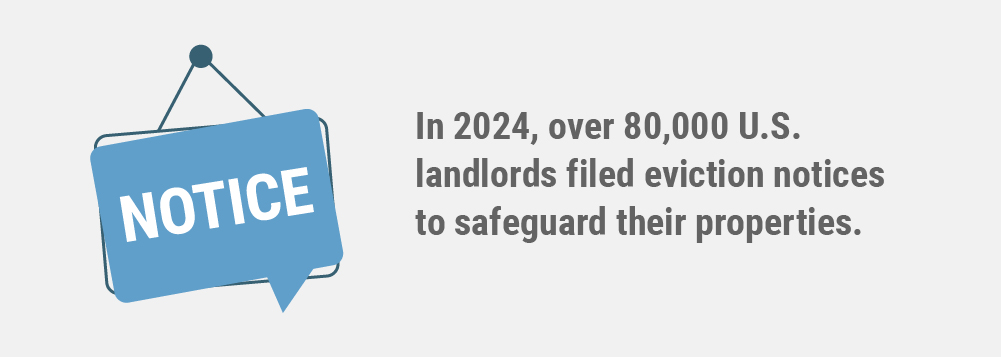

In 2024, around 80,000 U.S. landlords filed eviction notices to protect their properties for a variety of reasons. For example, in Oregon, 80% of those applications involved renters unable to make payments.

As a result, the actual cost of an eviction for a landlord is between $3,500 to $10,000, but can increase due to:

- Property turnover expenses

- Court fees

- Property damage

- Lost rent

- And other tenant-related liabilities

WHAT IS LANDLORD INSURANCE?

Insurance for landlords is specifically made for people who manage rental properties. In this case, our insurance teams individualize a plan that covers long-term property investors from losses associated with their rental portfolio, whether they are renting a single home or multiple apartments and buildings.

WHAT DOES A LANDLORD INSURANCE POLICY COVER?

Landlord insurance offers more comprehensive coverage than some believe. Given its affordability and the fortification of tenants’ rights ordinances and landlord lawsuits, these policies have become more needed than ever.

LEGAL EXPENSES

Including the legal expenses of an eviction noted above, landlord insurance offers liability coverage in case a tenant becomes injured, judgments resulting from tenant-caused property damage, and other qualified risks.

MEDICAL COSTS

The landlord’s job is to ensure a rental’s common areas stay safe, routine maintenance continues, and their home or apartment adheres to all state safety measures. In this case, a landlord insurance policy may reimburse you for medical payments you’re liable to pay if a tenant or their guest is injured on your property under eligible circumstances.

PROPERTY DAMAGE

It’s always challenging to hear landlords relay their issues with tenants who leave their properties in shambles. Unfortunately, property damage isn’t uncommon. In one survey on investment property damage, 21% of renters reported damages from mold, 21% from plumbing issues, and 7% due to structural problems.

In many cases, individualized landlord liability insurance mitigates financial losses from tenant-caused property damage. What’s more, a policy can also protect your investment during events like catastrophic weather events, vandalism, flooding, and fires.

LOSS OF RENTAL INCOME

Few landlords avoid gaps in rental income. Most tenant incomes aren’t catching up with rent increases, and climate change continues to place investment properties at risk.

When your rental property becomes uninhabitable, a landlord insurance policy might be your only resource for recouping lost revenue for an agreed-upon timeframe. In many cases, an insurance partner will assess your situation and recommend anywhere from a few months to a year—depending on your situation and risks.

IS LANDLORD INSURANCE THE SAME AS HOMEOWNERS INSURANCE?

No, both solutions address distinct needs.

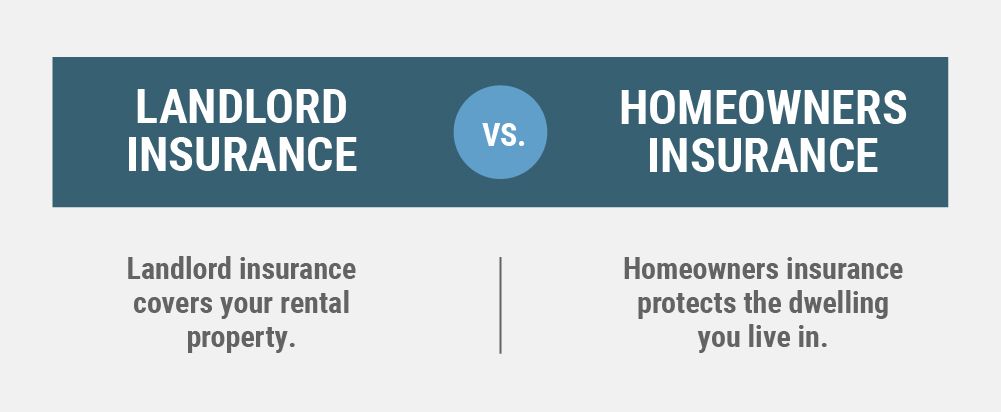

Homeowners insurance is essential for protecting the dwelling you live in, offering comprehensive coverage for both your home’s structure and personal property. It minimizes financial losses from unexpected events such as property damage and provides additional living expenses if your home becomes uninhabitable due to a covered event.

With customizable options, you can tailor your policy to include more extensive structural protection for owner-occupied homes, ensuring your investment is safeguarded against various risks.

Insurance for a landlord covers your rental property, whether you manage a building with several apartments, a single-family home, or a condo in a different state. Generally, this coverage sets it apart from homeowners insurance by offering:

- Loss of rental income coverage (in case your property becomes uninhabitable)

- Liability protection specific to landlord-tenant situations

- Coverage for certain tenant-caused damages

Keep in mind that you need to switch from a homeowners insurance policy to landlord coverage if you decide to move from your primary residence and rent it out.

PROTECT YOUR INVESTMENT WITH LANDLORD LIABILITY INSURANCE—GET A QUOTE TODAY.

We are a solutions-based insurance team operating nationally, curating various landlord insurance policies that comply with local regulations. Schedule a consultation with a landlord insurance professional to discover the difference partnering with a proactive team can make or to receive a curated quote. Once you connect with us, we’ll provide a detailed plan customized to your investment property portfolio, its risks, find ways to lower premiums, and more.

{kind=link}